The Double Tax Treaty between Cyprus and Austria contains a rather unique provision which allows Austrian residents to repatriate profits realized in Cyprus, back to Austria free of tax.

Article 8 of the Treaty provides that the profits from the participation as silent partner (Stiller Beteiligter) in a Cyprus legal entity are free from taxes in Austria.

This provision allows the minimization of the tax liability in Austria and in certain cases it allows the Austrian resident to pay no tax at all.

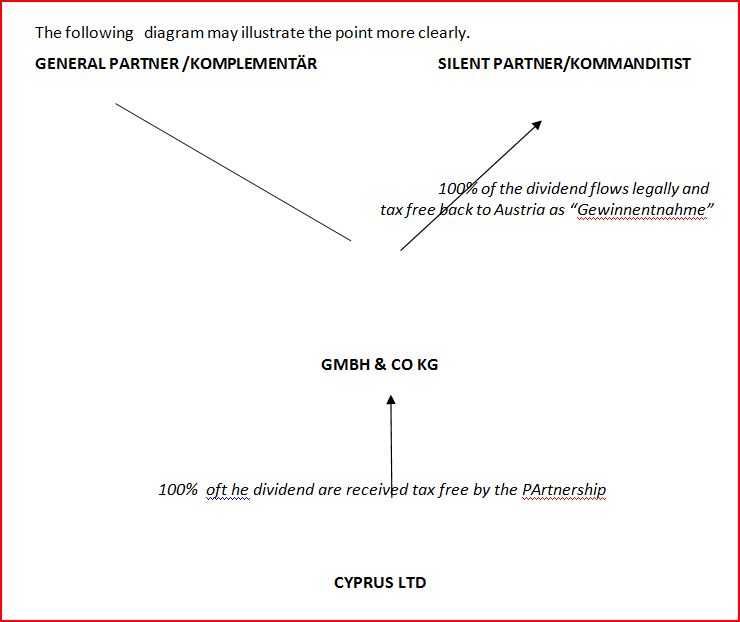

The first step is to create a Cyprus Partnership. This is similar in legal character to the Austrian Komanditgesellschaft. The General Partner (Komplementär) has unlimited responsibility while the limited or silent partner (Kommanditist) is liable only up to the amount of his contribution to the capital.

In order to limit the General Partner’s liability the role of the General Partner is undertaken by a limited company. The final form of the partnership can now be compared to that of a Gmbh & Co KG.

The Austrian National will be the silent partner i.e. the Kommanditist. The roe of the General Partner will be assumed by the Ltd which will be provided by our office against an annual fee. The General Partner will not participate in the profits .

As a second step the Limited Partnership incorporates a company, which I shall call for the purposes of this article the Active Company. The shares of the Active Company are held exclusively by the Partnership.

The active company is the company which is actively involved in the commercial activities, in short it is the company which is actually doing business.

The net profits of the Active Company are subject to tax at the applicable corporate tax rate in Cyprus,( currently at 10%).

After tax the profits are distributed by way of dividend payment to the Partnership. According to the law the dividends received by the Partnership are completely tax free.

The Partnership now will pay out to the partners their share of the profits (Gewinnentnahme). Thus the Austrian Partner (Kommanditist) receives his share of profits officially in Austria .. He will include it also in his tax declaration in Austria but the amount so declared is tax free in Austria. The only disadvantage is that it may push his income tax progressive scale a step higher.

Summarizing and concluding it may be said that the above method is an effective way of channeling profits from international operations back to Austria free from tax in a legal and transparent way.

The above described model has been tested successfully for the last three years both in Cyprus and Austria.

Additional Advantages

Making use of other Double Tax Treaties

The effect of the above mentioned advantages are amplified if one considers the additional benefits that can be reaped from the use of the Wide variety of Double Tax Treaties which Cyprus has concluded with large number of countries including the former former Eastern-Block Countries, the former Soviet Republics and Russia.

An interesting example is the Ukraine. The DTT between Cyprus and the Ukraine provides that the Ukraine will not impose any withholding tax on investments there. This in effect means that the profits from the Ukrainian investment are remitted to Cyprus in full and are taxed there at 10%

If the investor is an Austrian resident such profits can be remitted to Austria legally without being subject to Austrian tax as already explained in the preceding paragraph..

0% tax on profits from trading in securities.

The new tax regime in Cyprus provides that any profits derived from trading in securities, wherever in the world, are completely free of tax. Thus if the local branch of the bank trades with securities in Luxembourg for example, any profits derived from such trading are completely free of tax in Cyprus.

A resident of Austria wishing to trade with securities in the international markets can do this through a Cyprus company. The profits remitted to Cyprus are completely free of tax. Utilising the model described in the first paragraph an Austrian resident can ensure that these profits are legally remitted back to Austria free of tax.

0% Tax on Dividends

Dividends received by a Cyprus Holding Company from its subsidiaries or from investments in other companies are also free of tax. Thus if the Cyprus Cyprus company holds investments in other companies, wherever in the world situated, the dividends received from such investments are completely free of tax.